The rise of challenger banks

Over the past years, we have witnessed a steady rise of challenger banks, or neobanks. These newly established retail- and SME banks are challenging the established banks with modern banking propositions tailored to the digital world. In the aftermath of the financial crisis, many have been founded with the vision to create a better and more fair banking experience for customers.

Starting from scratch, they collectively managed to secure their position on the market and make a sizable impact. Our database of over 150 challenger banks worldwide currently counts a collective customer base of over 200 million customers, and still growing larger every month. Similarly, our Fincog Challenger Bank Index grew almost 8x larger since 2015, representing a growth of 55% per year.

One of the biggest success stories is Revolut from the UK. The company was founded in June 2013 and launched in July 2015 with foreign exchange services. Over time, it gradually expanded its offering to include amongst others current accounts and cryptocurrency trading. Nowadays it boasts a client base of 7 million customers.

Another success story is the Brazilian bank Nubank. It was founded in 2013 with the vision to bring simple and efficient financial services for Brazilian consumers to free them from existing high fees and unnecessary complexity. Nubank offers retail customer a free current account with a credit card and personal loans, combined with innovative financial management features. Since its initial launch in 2014, it achieved over 12 million customers in Brazil and is currently valued at $10 billion.

These success stories do not stand on their own. These challengers have appeared all over the world: for example Chime and Acorns from the USA, Toss and kakaobank from South-Korea, Judo Bank from Australia and WeBank from China, amongst others.

These challengers share some important commonalities. First, they have a strong focus on the digital world, and deliver advanced mobile apps with modern banking features – often only exclusively available through a mobile app. Not only the front-end, but also the back-end is largely automated, with minimum human interaction.

Second, they offer a great customer experience. The account opening process is simple and quick, daily banking services are easy to use and intuitive, and pricing is transparent. In addition, many offer financial management services (i.e. financial overview, savings tools) and seamless payments (i.e. instant P2P payments, mobile payments). Neobanks tend to focus on a specific customer segment or product, typically areas that are underserved or overpriced by incumbent players, with a better solution. Monese, for example, enables migrant workers to easily open a bank account, without the need of a postal address – which migrant workers may lack.

Third, they typically offer very competitive pricing to compete with established players. For example, many offer a free payment account, free or low cost international money transfers and travel money, and top rates on lending and deposits.

As opposed to incumbent players, neobanks are not hindered by legacy IT systems, large organizations, or physical distribution networks. Neither are they subject to the same regulatory requirements, as they often only provide a subset of banking services or operate under a different license (instead of a full banking license). In addition, they bring a fresh view and a new culture to banking, while focusing on the customer experience.

Collectively, the neobanks are making a permanent impact on the market, driving innovation and competition, setting the benchmark for incumbent players.

Low levels of income and profitability

While these challengers are successful in attracting large number of customers, many of them haven't quite yet made profit. Simultaneously, the larger the size, the more the losses.

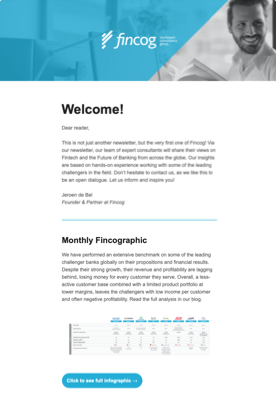

We have performed a benchmark on a selection of leading challengers internationally that are centered around payments (see infographic below). Over the years, they collectively secured a customer base of over 28 million Retail & Business customers. With a combined total funding of USD 2.9 billion, they are valued at USD 17.8 billion.

We have benchmarked them on their profile, propositions, pricing and financial results. What we observe is that all have negative profitability, losing money for every customer they serve. Monzo takes the bottom of the ranking with a total net loss of USD 58 mln (GBP 47.2 mln) in YE Feb-19, equivalent to a loss of USD 18.71 per customer. And as Monzo is growing, the losses only increase; the net loss increased from USD 37.6 (GBP 30.5 mln) in 2018, a rise of 54% YoY. Monzo is not alone; Revolut, N26 and the others also saw dramatic rises in their losses.

In terms of losses per customer, Nubank seems to be the closest to break-even, with a loss of (only) USD 2 per customer. The company has the highest number of customers in our sample, the most funding and highest valuation. Nubank’s income predominantly originates from credit cards, in which it secured its position thanks to a competitive interest rate, in combination with beneficial economic circumstances that drove customers to use credit cards as an alternative for consumer finance.

The large losses are predominantly driven by the bank’s low level of income. In our benchmark we measure total income net of the cost of sales, for example also subtracting the interest expense or commission expense to the total income. Mogo and Bunq achieve the highest income per customer, respectively USD 32.38 and USD 19.72. The income of the others is lower, for some even negative.

The low level of income can be explained by various factors. First of all, pricing is generally very competitive with thin margins. Second, they all offer only a sub-set of banking services, which limits their revenue potential. Third, while they generally do have a large customer base, a relatively large share is inactive and too often use it as secondary account.

The benchmark shows some important differences with incumbent players. Lloyds Banking Group (LBG) for example is one of the largest UK banks, serving over 30 million Retail and Business customers in the country, with a full range of financial service through a combination of both digital- and physical channels. Performing the same benchmark, it does have a much larger cost-base with operational cost of $335 per customer. However, with an income of $728 per customer, it achieves a profit of $180 per customer. Amongst others this is driven by a broader product portfolio and larger customer balances (i.e. around $18,200 in loans and $17,050 in deposits per customer).

This shows that the challengers still have a long way to go to deepen the customer relationship, to grow the revenue per customer and achieve profitability.

Some fundamental obstacles, but long-term success feasible

There are various reasons for the low profitability of the neobanks. First of all, many of the challengers are rather focused on growth of customers over profitability. Similar to the strategy of earlier Tech Giants, this approach assumes that they will find a way to capitalize on the large customer base later on.

For example, N26 caught lots of attention after its latest funding round in July 2019 when co-founder Maximilian Tayenthal stated that profitability was not one of their core metrics. Tayenthal said: “We want to build a global financial services company… In the years to come we won’t see profitability, we’re not aiming to reach profitability. The good news is we have a lot of investors that have very deep pockets and that share our deep vision.”

Two years ago the CEO of Monzo, Tom Blomfield shared a similar view: “The more you grow, the more you lose and you have to turn that corner at some point… Getting to profitability is not a goal we are prioritising over delivering customers real value. If that takes 10 years, we are committed to it.”

It is true that most challengers are still relatively early phase and operating at subscale. They require large initial investments to build the company and in marketing to attract customers. Once they have established their foundation with sufficient economies of scale, they should be better positioned to be profitable.

What makes it more difficult to achieve this is that the challengers must compete with existing banking infrastructure and banking relationships. Churn-rates in banking are rather low, depending on the market, typically around 2-5% per year. Many struggle to secure the primary customer relationship, which is the most sticky and most profitable one, and offers the best opportunities for cross-sell. Instead, customers more often use the neobanks as secondary accounts for specific services or features.

This requires the challengers to offer large incentives for customers to switch banks, being a better service or price. And in fact that is the strategy of most challengers who offer very competitive pricing, with free payment accounts, low-cost international transfers etc. Moreover, charging customers for certain services is consider unfair, ‘ripping off customers’. This leaves many of them with tiny – or even negative – margins on their services.

Last, most challengers still offer a rather limited product portfolio, typically centered around the payment account only. Especially when the core services are offered for free, this provides few options to generate substantial income. Many of the UK challengers, for instance, have largely relied on interchange fees on card payments, but this now seems to be an insufficient source of income on its own. As opposed to most incumbent players that offer a full range of banking services and can benefit from cross-sell opportunities to achieve much higher revenue per customer.

Overall, the less-active customer base combined with a limited product portfolio at lower margins, leaves many challengers with rather low income per customer and often negative profitability.

This may spark the question whether these challengers are able to survive in the long-run, to achieve sufficient scale and become profitable. Surely not all will survive, in fact we already have witnessed the end of various players, such as Hufsy (Denmark) that recently ceased operations.

However, we believe that with the right strategic choices challenger banks should be able to enhance their profitability, achieving a sustainable business model with a lasting positive impact on customers. In our next blog we will share some insights on challengers that are profitably, what we can learn from them and how to improve your own profitability.

Click on the link or picture for a high-quality version of our benchmark